When a parent or loved one begins to need extra support, one of the first questions families face is how funding for care works in the UK. It’s rarely something anyone has planned for, and the system can feel difficult to understand, particularly when these stressful decisions must be made alongside work and other responsibilities.

The good news is that support is available regardless of your financial situation. Whether you have significant savings or limited means, there are pathways to ensure your loved one receives the care they need. At Serene Care Group, we believe that understanding your options is the first step toward making informed decisions with confidence.

This guide explains how the UK care funding system works, from the basic distinction between NHS and social care through to practical steps you can take today.

Understanding the basics: NHS care vs social care

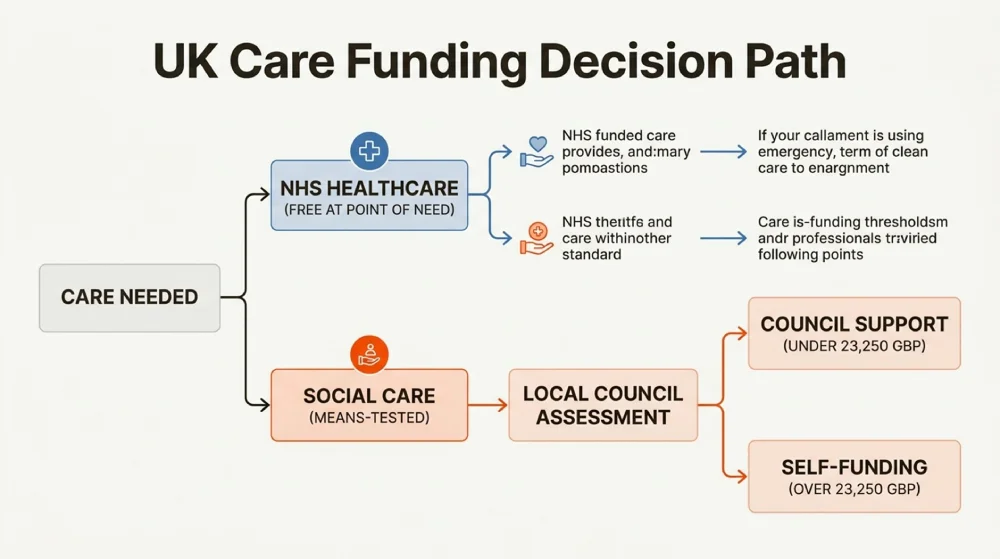

The foundation of understanding care funding is recognising the critical distinction between NHS healthcare and social care. This boundary determines who pays for what, and it’s where much confusion arises.

NHS healthcare is free at the point of need, regardless of your financial situation. This includes hospital treatment, GP appointments, ambulance services, and nursing care provided in NHS settings. If your loved one’s needs are primarily health-based, the NHS may fund their care entirely.

Social care is means-tested. This covers help with daily living activities such as washing, dressing, meal preparation, mobility assistance, and supervision. It also includes residential care in a care home. Unlike NHS healthcare, social care funding depends on your financial circumstances.

The concept of “primary health need” determines whether someone qualifies for NHS Continuing Healthcare (CHC). If the majority of a person’s care involves managing health needs rather than social or personal care, they may be eligible for fully funded NHS care. This isn’t based on their diagnosis but on the nature and complexity of their needs.

Many care homes provide both nursing care (healthcare) and personal care (social care), which is why funding arrangements can become complex. A resident might receive NHS-funded nursing care for medical needs while paying for their accommodation and personal care.

The means test: How your finances affect care funding

For social care, the local authority conducts a financial assessment to determine how much you can afford to contribute. This assessment follows clear national rules, though the details can feel overwhelming at first.

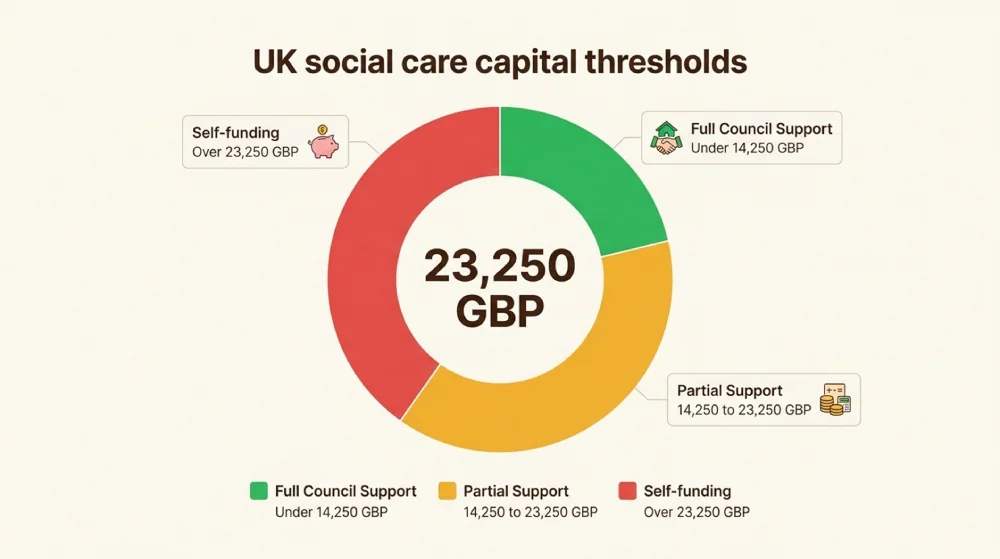

The £23,250 threshold is the key figure to remember. In England and Northern Ireland, this capital limit determines your eligibility for council support:

Your capital | What you will pay |

Over £23,250 | Full cost of your care (self-funding) |

£14,250 to £23,250 | Council contributes, you pay from income plus tariff income |

Under £14,250 | Council provides maximum support, you pay only from income |

What counts as capital? Savings, investments, stocks and shares, land, property (in some circumstances), and premium bonds. If you have joint finances, such as a savings account with your partner, it’s assumed you have an equal share unless you can prove otherwise.

What’s disregarded? Certain disability benefits, the value of your home if you receive care at home, personal possessions, and household goods. The first £100 of occupational pension income is also typically disregarded.

Tariff income applies if your capital falls between £14,250 and £23,250. For every £250 (or part of £250) you have above £14,250, you’re assumed to have £1 per week in additional income. So if you had £15,000 in savings, you’d pay an extra £3 per week toward your care.

Personal Expenses Allowance: Even if you receive full council support, you must be left with at least £30.15 per week for personal expenses. The council has discretion to increase this amount depending on your circumstances.

Regional variations exist across the UK. In Wales, the threshold is £50,000 for care home fees. In Scotland, the upper limit is £35,000 with a lower limit of £21,500. These differences reflect the devolved nature of social care policy.

Getting assessed: The two-step process

Accessing care funding requires going through two separate assessments. Understanding what each involves helps you prepare and reduces anxiety about the process.

Step 1: Care needs assessment

Everyone is entitled to a care needs assessment regardless of their wealth. This evaluation determines whether your needs meet the national eligibility criteria and what level of support you require.

The assessment considers your ability to carry out daily activities, risks to your wellbeing and safety, and how your condition affects your independence. A social worker or care professional will visit you at home or in hospital to conduct the assessment, which may involve discussing your needs with you, your family, and any existing carers.

You can request a care needs assessment by contacting your local council’s adult social services department. There’s no charge for this assessment, and you have the right to have someone with you during the process.

Step 2: Financial assessment

If the care needs assessment identifies eligible needs, a financial assessment follows. This means test determines how much you can afford to contribute toward your care costs.

To prepare, gather information about all your accounts and income sources. This includes savings accounts, investments, property deeds, pension statements, and benefit award letters. You should also document any disability-related expenses you have, as these may be taken into account.

The assessment typically takes a few weeks to complete. Once finished, you’ll receive a letter explaining the cost of your care and how much you need to pay. If you disagree with the decision, you have the right to ask for an explanation and to challenge it through the council’s complaints procedure.

While waiting for assessments to be completed, it’s worth exploring whether any interim support is available, particularly if your needs are urgent.

NHS Continuing Healthcare: When the NHS pays for everything

NHS Continuing Healthcare (CHC) is a package of care arranged and funded by the NHS for individuals with significant ongoing health needs. Unlike social care, CHC isn’t means-tested. It’s available regardless of your income or savings.

What CHC covers:

- Care home fees, including accommodation costs

- Home care services

- Supported living arrangements

- Personal care and healthcare needs

Who qualifies?

Eligibility depends on having a “primary health need” rather than a diagnosis. The assessment looks at the nature, complexity, intensity, and unpredictability of your needs. Conditions that might qualify include advanced dementia with challenging behaviour, severe neurological conditions, or rapidly deteriorating health.

The assessment process:

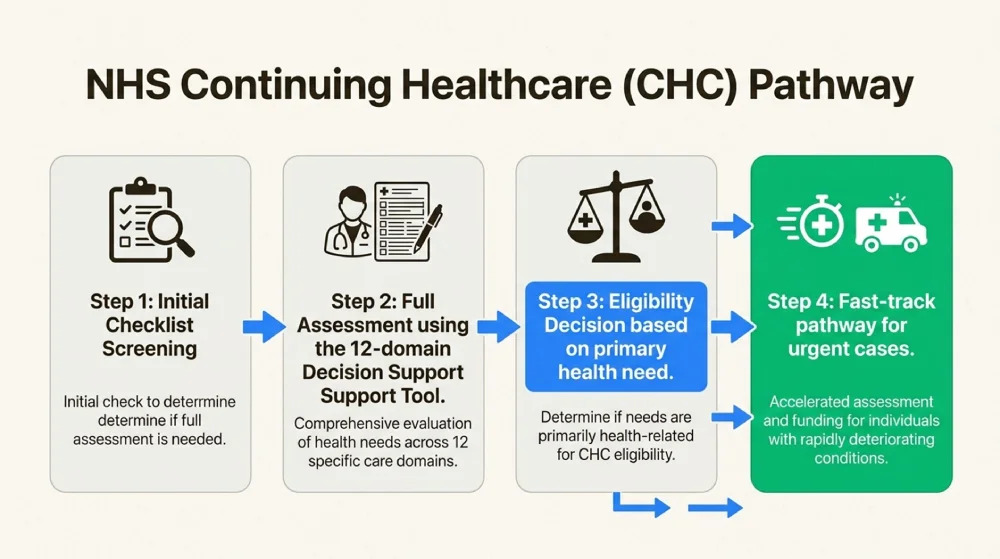

- Initial checklist: A nurse, doctor, or social worker completes a screening tool to determine if a full assessment is warranted.

- Full assessment: A multidisciplinary team uses the Decision Support Tool to evaluate your needs across 12 domains, including behaviour, cognition, psychological and emotional needs, communication, mobility, and nutrition.

- Decision: If you have at least one “priority” need or multiple “severe” needs, you should qualify for CHC.

- Fast-track pathway: For those with rapidly deteriorating conditions who may be nearing end of life, a fast-track assessment can provide immediate funding.

NHS-funded nursing care: If you don’t qualify for full CHC but need nursing care in a care home, the NHS pays a standard rate of £254.06 per week directly to the nursing home. This reduces the amount you pay in fees.

To request a CHC assessment, ask a GP, social worker, or district nurse to arrange an initial screening. The charity Beacon provides free independent advice on NHS Continuing Healthcare and can be contacted on 0345 548 0300.

Property and care funding: Will you have to sell your home?

The family home is often the biggest concern when considering care funding. Many families worry they’ll be forced to sell their property to pay for care. Understanding the rules around property can provide significant reassurance.

When your home IS counted in the financial assessment:

- You’re moving into residential care

- The property is solely in your name

- No qualifying relatives live there

When your home is DISREGARDED:

- Your spouse or partner still lives there

- A relative aged 60 or over lives there

- A disabled relative lives there

- Your child under 18 lives there

- Your ex-partner lives there as a lone parent

- You’re receiving care in your own home

Deferred Payment Agreements: If most of your assets are tied up in your property, you can ask your local council for a deferred payment agreement. This means the council effectively lends you the money to pay for your care costs, and the debt is repaid when your home is eventually sold. Interest is charged on the deferred amount, but this option allows you to retain ownership of your property during your lifetime.

12-week property disregard: When you first enter a care home, the value of your home is disregarded for the first 12 weeks. This gives you time to sell the property or arrange alternative financing without immediately having to fund the full cost of care.

Important reassurance: Local authorities can’t force you to sell your home during your lifetime to pay for care. While the value of your property may be included in the financial assessment, you have options for managing this without an immediate sale.

Benefits that can help with care costs

Even if you’re self-funding your care, you may be entitled to benefits that aren’t means-tested. These can provide valuable additional income toward care costs.

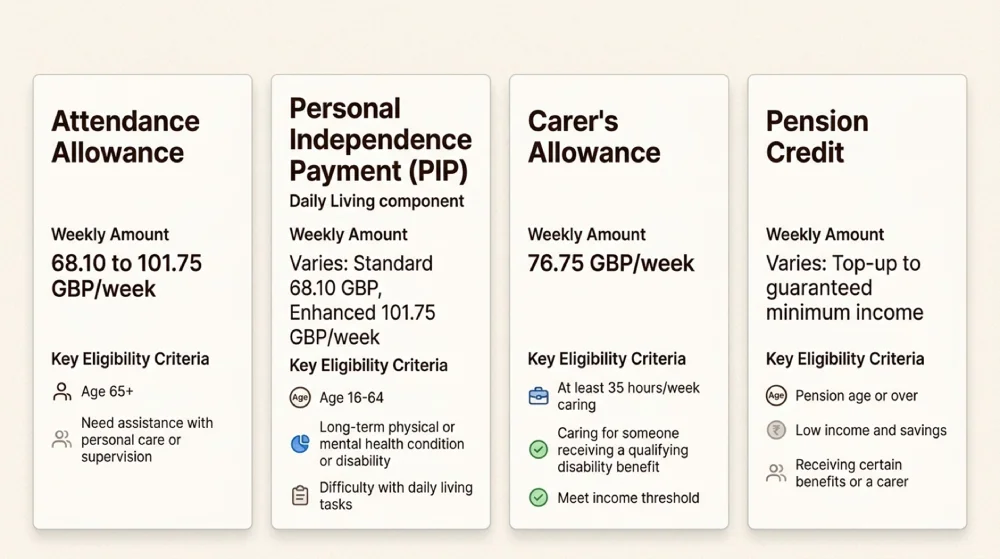

Attendance Allowance:

Available if you’re over State Pension age and need help with personal care due to illness or disability.

- Lower rate: £68.10 per week (for day or night care)

- Higher rate: £101.75 per week (for day and night care)

You must have needed help for at least six months to qualify. Attendance Allowance isn’t means-tested, so your savings don’t affect eligibility. You can use this money however you choose, including toward care costs.

Personal Independence Payment (PIP):

For those under State Pension age with care needs:

- Daily Living Component: £68.10 to £101.75 per week

- Mobility Component: £26.90 to £71.00 per week

Carer’s Allowance:

If someone provides significant unpaid care for you, they may qualify for Carer’s Allowance of £76.75 per week. They must care for you for at least 35 hours per week and earn less than £139 per week after deductions.

Pension Credit:

Tops up your weekly income if you’re on a low income and over State Pension age. It can also unlock other benefits such as housing benefit and council tax reduction.

How benefits interact with care funding: Attendance Allowance and PIP are disregarded in the financial assessment for care, meaning they don’t reduce your council support. However, they can be used to help pay for care costs or other expenses.

Self-funding your care: What you need to know

If your savings exceed £23,250, you’ll be expected to self-fund your care. This gives you greater choice and control over your care arrangements, but it also comes with responsibilities.

Managing your care arrangements:

When self-funding, you can choose any care home willing to accept you. You’ll enter into a contract directly with the care provider. Ensure the contract clearly states:

- What services are included in the fees

- What might be charged as extras

- How much notice will be given if fees increase

- The notice period required if you wish to leave

What happens when savings run out:

If you’re self-funding and your capital approaches £23,250, contact your local council about three months before you expect to reach this threshold. Request a new financial assessment. The council must arrange this promptly so you don’t have to use up your capital below the threshold amount.

Once your savings fall below £23,250, the council may assist with funding. They’ll need to confirm you still need care in a care home through a care needs assessment if one hasn’t been done recently.

Top-up fees: If you prefer a care home that costs more than the council’s standard rate, a third party (usually a family member) can pay the difference. This is called a “top-up” fee. The council can’t ask for a top-up if you’re in a more expensive home out of necessity rather than preference.

Getting help and next steps

Navigating care funding is complex, but you don’t have to do it alone. Several organisations offer free, impartial advice to help you understand your options.

Free sources of advice:

- Age UK: Offers a national advice line and local branches providing face-to-face support

- Citizens Advice: Free, confidential advice on benefits and care funding

- MoneyHelper: Government-backed guidance on paying for long-term care

- Beacon: Specialist advice on NHS Continuing Healthcare

When to seek professional advice:

Consider consulting a specialist care fees adviser or solicitor if:

- Your financial situation is complex

- You have inheritance planning concerns

- You’re in dispute with your local authority

- You need advice on deprivation of assets rules

Important documents to organise:

- Lasting Power of Attorney (if not already arranged)

- Financial records and bank statements

- Property deeds

- Benefit award letters

- Pension statements

Your next steps:

- Request a care needs assessment from your local council

- Gather your financial documents together

- Check your benefit entitlements using online calculators

- Research care options in your preferred area

- Consider seeking independent financial advice if your situation is complex

At Serene Care Group, we understand that navigating care funding can feel overwhelming. Our team is here to provide transparent, compassionate guidance to help you understand your options. Whether you’re self-funding or accessing council support, we believe everyone deserves high-quality care that preserves their dignity and supports their independence.

If you’re considering care for yourself or a loved one, we encourage you to reach out. Understanding how funding for care works in the UK is the first step toward making informed decisions that provide peace of mind for the whole family.

Frequently Asked Questions

How does funding for care work in the UK if I have savings above £23,250?

If your savings and capital exceed £23,250 in England, you are considered a self-funder and will pay the full cost of your care. However, you should still request a care needs assessment to confirm the type of care you require. You can also claim non-means-tested benefits like Attendance Allowance to help with costs. Once your savings fall below £23,250, contact your local council to request a financial reassessment.

Will I have to sell my house to pay for care if I need residential care?

Not necessarily. While the value of your home may be included in the financial assessment for residential care, there are several circumstances where it is disregarded. These include if your spouse or partner still lives there, a relative over 60 lives there, or a disabled relative lives there. Additionally, Deferred Payment Agreements allow you to delay selling your home, with the council paying your care costs and recovering the debt when the property is eventually sold.

How does NHS Continuing Healthcare funding work alongside local authority care funding?

NHS Continuing Healthcare (CHC) covers the full cost of care for those with a ‘primary health need,’ including accommodation costs if in a care home. It is not means-tested. If you qualify for CHC, the NHS funds everything and local authority funding is not needed. If you do not qualify for full CHC but need nursing care, you may receive NHS-funded nursing care of £254.06 per week, with the remainder potentially covered by local authority funding or self-funding depending on your means.

What benefits can I claim to help with how funding for care works in the UK?

Several non-means-tested benefits can help with care costs. Attendance Allowance provides £68.10 to £101.75 per week for those over State Pension age who need personal care. Personal Independence Payment (PIP) is available for those under State Pension age. If someone cares for you for 35+ hours per week, they may claim Carer’s Allowance of £76.75 per week. These benefits are disregarded in the care funding assessment, so they do not reduce your council support.

Can I give away my assets to avoid paying for care?

Giving away assets to avoid care fees is known as ‘deprivation of assets.’ If your local council believes you have deliberately transferred assets to qualify for funding, they may assess you as if you still own those assets. This is called ‘notional capital.’ There is no time limit on how far back councils can look, so this strategy is risky and could leave you without funds when you need care. Always seek professional advice before making significant financial transfers.

What happens to my care funding if my needs change?

If your care needs change, you can request a new care needs assessment at any time. If your financial situation changes, such as inheriting money or your savings falling below the threshold, you must inform your local council as this may affect your contribution. The council is required to review your care needs and finances regularly, typically annually, to ensure your support remains appropriate.